Valuing New-Build Property.

In this article we explore the approach to valuing new-build residential property being sold for the first time (this includes actual ‘newly built’ property as well as new conversions etc.).

This is an area that is getting more complex. The valuation of a new-build property should be approached in a similar way to any other valuation; however, there are specific aspects of the new-build residential market that require additional consideration and analysis by the valuer.

Definition of new-build property

What is the definition of a new-build property in the residential context?

Generally, it is a property that has been newly constructed and is to be occupied for the first time as a dwelling. However, you should be aware that some lenders apply a different definition of new build, and some may include a property up to 1 year and in some cases 2 years old. After that time, it is not considered a new-build property, even though it has not been occupied.

A property is also classed as a new build if it is a conversion from another use and if it has not yet been occupied, for example, a barn converted to a house.

New-build properties usually have a form of warranty: in effect an insurance designed to ensure the original builder fixes any problems that may arise. The most common warranty is the NHBC, but there are other warranty schemes, and warranties do vary. The usual period of cover is 10 years, but some warranties do offer cover for a longer period.

Valuation

The valuation of individual new-build homes requires an understanding of issues that are unique to this sector of the residential market.

Issues range from having an appreciation of the physical attributes of new property and how these may add value above that of a similar property in the resale market, to having an awareness of the marketing techniques used by house builders and understanding as to how such techniques might impact on the selling price of a new-build home.

You may also come across a development, usually one that is of a reasonable size, where the developer uses ingenious marketing techniques not available in the second-hand market to make sure that the homes they build are being sold. This may include a range of incentives designed to promote property sales. Furthermore, there is also the governments ‘Help to Buy’ scheme. All these additional factors must be taken into account when valuing a new-build property.

RICS

As you would expect, the RICS provides guidance on the valuation of new-build properties. The latest guidance is Valuation of individual new build homes – 3rd Edition, December 2019.

As well as the specific guidance note mentioned above, there is reference to VPGA 11.4 UK 2017 (which has almost superseded Appendix 10 of the Red Book).

So, what makes the new-build market so special, and why does the valuer have to approach this with care?

As the RICS ‘Valuation of new-build homes 3rd Edition’ guidance document notes:

“The valuation of residential property for mortgage purposes is well understood, but the new-build sector is constantly evolving and becoming increasingly complex.”

Let us consider what some of these issues might include:

Physical attributes, for example:

o Floor layout in line with modern aesthetics etc.

o Ability of the purchasers to choose certain fixtures and fittings (bathrooms, kitchens etc.)

o Energy efficiency: potentially cheaper to run than similar properties in the resale market.

o Occupancy safety: built to modern building regulations.

o In theory, no repairs will be needed in the short to medium term.

Marketing techniques: developers can employ different techniques to those used by agents in the resale market. These may have an impact on the selling price of a new property.

• Specific market product and policies from lenders: individual lenders take a varying approach to brand new homes; it is all about risk and some lenders are in the ‘low risk’ loans. Their approach will be different to a lender that is less risk averse. Some may refuse to lend on certain properties whilst others may be happy to loan and some will insist on a larger deposit. No two lender’s policies or deals will be the same. Also, lenders will not want to be over exposed on a new development and may restrict the volume of lending on a particular development.

• Purchaser aspirations: despite some recent bad press around new-build property and the fact that the RICS and others are looking at snagging/defects, many consumers are not aware of any potential ‘down side’ and prefer new build over a similar second-hand property. It is important for valuers to be alert to changing attitudes to issues which may have particular consumer appeal such as:

o Environmental impact of buildings.

o Efforts to reduce carbon emissions.

o Use of innovative forms of construction.

o What is often described as a ‘new-build premium’.

Where public perception on these matters is reflected in market demand, the new-build property may, and often will, attract added value in comparison with the second-hand market.

• The strength of the builder in transactions and how they can control supply: while smaller development projects do exist, firms like Taylor Wimpey build several thousand homes a year (Taylor Wimpey claims over 10,000 units a year on its website).

• Restricted transparency in pricing.

• Re-generational effects of some new schemes – there is a logic that would suggest that if an area is ‘run down’ with economically unviable buildings which are in a poor state of repair and subject to vandalism etc. then by definition new housing will ‘improve’ that area. However, the suggestion that developments quickly blend into the wider housing market is not a given, and re-generational effects must be approached cautiously.

Conversions under permitted development (for example from buildings previously used as offices, industrial and agricultural usage). However, there are issues that a valuer should consider which are specific to these conversions. For example:

o Access shared with commercial or industrial property.

o For flat conversions from 1960s and 1970s office buildings, the unknown condition of the underlying concrete construction (for example, old concretes can contain damaging constituents such as High Alumina Cement, Chlorides or Sulphates).

o The condition of the steel reinforcement inside the concrete.

o Will the conversion be resaleable in the future?

o Is there a mix of residential use within the area, or is the conversion in a non-residential area?

o Is there an appetite from lenders for this type of conversion? For example, some lenders will not lend on office to residential conversions.

o Linked to the above, is there sufficient residential infrastructure in the immediate area, e.g. access to amenities/shops/schools/transport?

• Government intervention into the market: Help to Buy, or Starter Home schemes can skew the market.

• Planning conditions: for example, Section 106 agreements, resale restrictions or social housing mix requirements.

• Innovative forms of construction and specific eco-features that may be included.

New-build premium

The term ‘new-build premium’ is a term that is used to indicate any ‘additional sum’ that a purchaser is prepared to pay for a residential property that has not previously been occupied. In other words, it is a premium that may be attributable to features that are unique to new-build properties.

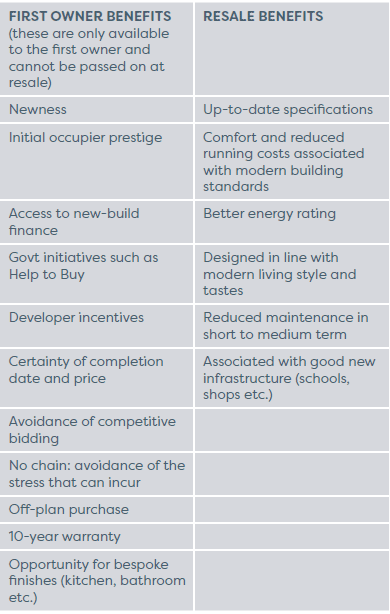

These features fall into two categories:

A new-build premium is not universally found (especially where there is a plentiful supply of new property), but it is relatively common in particular sectors, or locations, and relates entirely to the first occupation of a property (or ‘first owner benefits’).

Care should be exercised in the understanding and use of this term. While a component of market value, it does not relate to additional value arising from physical attributes that will remain after first occupation and which may add value on subsequent resale. Hence it can cause confusion and the term ‘first owner benefits’ is more appropriate than that of new-build premium.

Dealing with assumptions

UK VPGA 11 in RICS Valuation – Global Standards: UK national supplement 2018 (Red Book), and the RICS residential mortgage specification set out a number of standard assumptions and special assumptions that are included in the terms of engagement agreed with UK lenders, though it should be noted that not all lenders have agreed to follow the mortgage specification.

For new-build property it should be noted that, unless instructed otherwise, the following assumptions and special assumptions will be made:

• If the building has not yet been finished, the valuation will be made on the ‘special assumption’ that the property being valued has in fact been satisfactorily completed, as at the date of the inspection, and has been done so fully in accordance with planning permission and other statutory requirements.

• The valuation will be based on the assumption that the property has been built under a recognised builders warranty or insurance scheme approved by the lender or that it has been supervised by a professional consultant capable of fully completing the Professional Consultants Certificate to meet lender requirements.

• If the subject property forms part of a complex which, when finished, will have certain communal facilities such as communal parking areas, communal gardens etc., then the valuation will assume that these facilities have been completed to the appropriate standard if they have not been completed at the date of the valuation.

• The same applies to any planned infrastructure to be included as part of the development, for example, transport links, retail units etc.

• In some cases, lenders will require RICS members to assume that the new-build property is already occupied. (If a lender requests that this or a similar special assumption be adopted, guidance should be obtained from the lender specifying how their instruction is to be interpreted; for example, a lender may require second-hand or resale value.)

UK VPGA 11 allows valuers to make assumptions relating to the lease term, service charge, repairs, and ground rents. However, this is increasingly a very tricky area. In recent years there has been a lot of bad press around the sale of leasehold houses on particularly onerous ground rent terms. Some lenders are now stipulating that ground rent terms must be ‘reasonable’ during the term of the lease. Consequently, the valuer cannot just make assumptions around lease terms anymore and can expect that they will need to obtain more information before the value can be determined. Valuers should also be aware of service charges imposed on the freeholders of houses for the upkeep of the estate, as estate roads, lighting and communal areas are less likely to be adopted by local authorities (this information will usually be provided on the UK Disclosure of Finance Form, known as UKDIF).

Development sites and development plots

Ideally, as with all valuations, the valuer would visit the subject property. But with new-build properties, this is not always so straightforward. For example, the property being valued might not actually be built, and access to the site is often restricted for health and safety reasons. In that case, it is possible to undertake a valuation, but care must be taken to document and record what information was referred to in determining the valuation. This record will include the sources of any assumptions made. For example, the location of the subject property will be one such assumption. For this it is not sufficient to rely on the marketing material produced to promote the site and the individual units. Instead, construction site plans and detailed builder specifications must be used to determine the location and finish of the property being valued. These will be acceptable sources of information used to validate assumptions. Where possible, the show home should be visited (and that visit recorded) and a similar unit inspected.

Great care must be taken to ensure that the location of the subject property is clear. The same units on different areas of a larger site are not necessarily the same value. Just as with second-hand properties, the location will play an important factor. Location features such as proximity to a main road, school or other local facility may have an impact on value, as might proximity to, for example, a social housing element on a mixed tenure site.

Another consideration is the use of the whole site before redevelopment for housing. It cannot be assumed, even in a rural location, that the previous use of the site (whole or site) was simply ‘grassland’. Particularly in urban areas there are construction sites which may have had a previous use that contaminated the land in some way, having potential implications on the value.

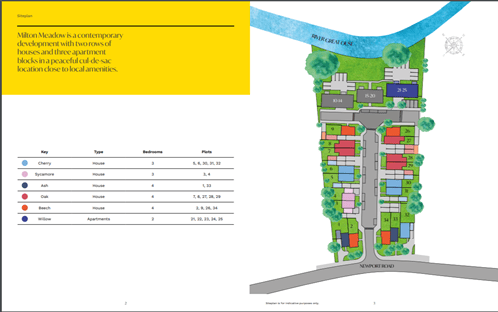

Figure 1 – Milton Meadow, development plan.

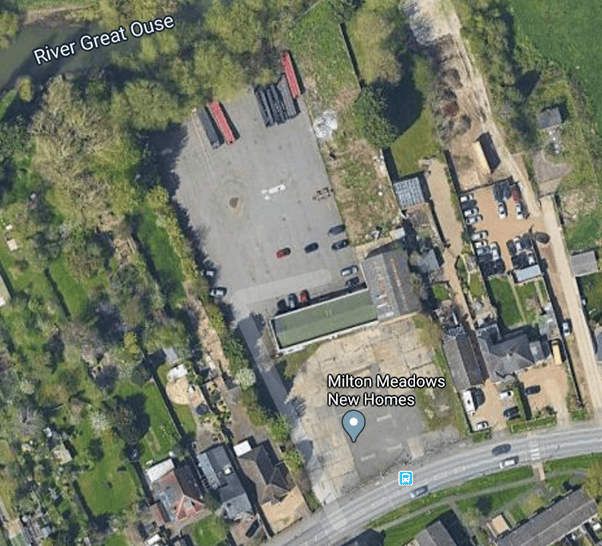

Figure 2 – Milton Meadow site from Google Earth showing development was on a site previously developed for commercial purposes.

Determining the value

There are three key things to consider when determining the value of new-build properties; (1) what is the wider market doing, (2) identifying and analysing the appropriate comparables and (3) the interpretation of those comparables to establish the market value.

The wider residential property market is complicated at the best of times, and at the time of writing this article we are in completely uncharted territory when it comes to the knock-on effect of the COVID-19 pandemic (both authors are ‘working from home’). That aside, if it were as simple as many agents or commentators would have us believe, why do businesses like Knight Frank and Savills spend so much money on expensive research teams? Valuers must interpret the market in which they are valuing, so it goes without saying that valuers must be aware of national market trends as well as local issues.

One thing to consider with new-build properties is whether the development on which the subject property is located may be ‘skewing’ the market at a local level. An example of this might be the new Waterbeach development in South Cambridgeshire. In 2019 planning consent was granted for 6,500 new homes on a disused military site. Waterbeach is currently a ‘satellite’ village for Cambridge. This development will inevitably completely swallow the original housing. Via Section 106 agreements, the development is planned to include a lot of new amenities both for the development and surrounding areas, but these amenities will not all be delivered at the same time. The authors believe that the new town at Waterbeach will inevitably skew the local market, but not necessarily immediately. Only time will tell how much this development lives up to the initial promise.

Well-planned developments can, and do, bring brownfield sites and underused, out of date industrial and commercial property into new use with sustainable value, but this is not always the case. Examples of where things can ‘go wrong’ are overdevelopment, the wrong phasing of amenities and a property type mix that does not match local demands. For example, in January 2018 The Guardian reported:

“More than half of the 1,900 ultra-luxury apartments built in London last year failed to sell, raising fears that the capital will be left with dozens of ‘posh ghost towers’”.

There are also the conversions that look great but do not meet many lenders requirements and will therefore struggle to obtain mortgage lending, particularly for the owner-occupier market. An example of this is an office conversion in Essex where many of the flats face into an enclosed atrium and have no or limited external window openings.

When it comes to comparables, the Red Book makes it clear that “…valuing a new-build property should be approached in the same way as any other valuation.” But it then goes on to say, “In all instances, the notified sale price must be treated with caution”. (UK VPGA 11.4 in RICS Valuation – Global Standards: UK national supplement 2018)

What does this mean in practice?

Of course, in theory, following the normal logic that ‘the property geographically closest to the subject property and offering the same features sold nearest in time to the valuation will be the best comparable’, then sales on the same development will be the best comparables. However, we have already mentioned that the development itself might be skewing the market, so might it also potentially skew the comparables?

Consider the way developers offer homes for sale. They tend to use marketing techniques far more sophisticated than those seen in the usual resale market,

such as contributions to stamp duty, help with deposits or extras in the property over and above that in the standard specification. But often these are individual to the plot and what is offered may depend on the position in time of the life cycle of the development. Then there are the various incentives such as Help to Buy. Conversely, some lenders might have stopped lending on certain sites because they are over exposed (depending on their own risk profile and strategy) and that could limit the access to available funding. What impact will that have on value?

Comparables from the same site alone are insufficient. Instead, comparables should ideally include:

• New build but on a different nearby site (not so problematic is a city such as Milton Keynes with a lot of development, but potentially much more difficult in a green belt area like South Cambridgeshire where the new Waterbeach town is planned).

• A similar property from the resale market.

If comparables from a seemingly similar nearby site are available, then it cannot be automatically assumed that they will be ideal. Are the sales techniques the same? Are the developers offering different incentives? Are the tenures and property mix similar? Is the access to amenities similar?

The Milton Meadow site in Milton Keynes (see figure 1 and 2) is a good example of this analysis. The developer is not a large volume house builder normally associated with Milton Keynes, but a much smaller local developer. Can they offer the same incentives? Is their marketing strategy and budget similar? The site also has more ‘radical’ house designs than other new sites in the area. How might this impact on the value of the houses here? And, as we saw above, the site is a former commercial property. Unlike many new sites in Milton Keynes, it is not a green field development. Will this impact on the value? Careful analysis is required and must be recorded.

The resale market also requires additional scrutiny. We know that new-build properties include features that are simply not available in the resale market. Often referred to as a new-build premium, when analysing comparables, it is much more useful to consider these features as ‘first owner benefits’. These are ‘benefits’ that simply cannot be transferred to the second owner (or indeed found in the resale market in general). Examples include the ability for the purchaser to specify finishes, first owner ‘prestige’, avoidance of ‘housing chains’ etc. It is usually assumed that such benefits will add value to a new-build property but how much value, if any, can actually be attributed to them?

Conversely, resale properties might have an intrinsic value that cannot be assumed for the new site. For example, a comparable family size home in the resale market may be in the established catchment area of a local school that has an excellent reputation. However, there is no guarantee that the catchment area will extend into the new development. How then might this impact on the attractiveness of two very similar family homes? Will the school catchment ‘trump’ the first owner benefits of the new house?

Figure 3 – New homes at Milton Meadow

Conclusions

Valuing new-build property is tricky and needs to be approached with care, with the valuer ensuring that they record all relevant matters and carefully analyse the comparable evidence before reaching their conclusion on value. We hope this article goes some way to illustrating some of the complexities involved. Anyone involved in such valuations must read the RICS guidance note 3rd Edition, the Red Book and of course, the guidance produced by any lender that they are providing valuations for

Anne Hinds BSc (Hons) FRICS is a Chartered Surveyor dealing with technical advice and guidance on mortgage valuations, expert witness reports and other survey and valuation matters. Qualifying in 1986 she originally worked in the industrial and commercial sector followed by a period in the Valuation Office before moving into residential with Legal and General Surveying Services, eventually becoming National Quality Assurance Surveyor. She then went on to become Customer Care Director with the surveying division of the Spicerhaart Group and later esurv. For several years Anne has worked with a small firm carrying out mortgage valuations and residential surveys along with expert witness and other surveying related matters. She is now the Risk and Technical Manager for Kinleigh Folkard and Hayward Chartered Surveyors. With over 30 years’ experience in surveying, primarily in the investigation, management, and handling of negligence claims against surveyors, Anne is well aware of the measures that should be taken to ensure good risk management within firms. Anne is chair of the RICS Assigned Risks Panel, she has sat on the RICS Residential Survey and Valuation Group, has been involved with several information papers including the valuation of individual new build homes and is a former chair of the RICS Disciplinary Panel. Anne has been involved with Sava since its inception and undertakes assessment for those wishing to qualify as AssocRICS surveyors.

Hilary Grayson BSc EST MAN (Hons) is Director of Surveying Services at Sava and is focused on developing new qualifications, as well as Sava’s activities within residential surveying. Hilary has a wealth of experience within the built environment, including commercial property, local government and working at RICS.

Are you an experienced Residential Surveyor?

We are looking for part-time, freelance Assessors for our Level 6 Diploma in Residential Surveying and Valuation. Being an assessor is a flexible role which can fit around your existing surveys and commitments.

Sava Assessors contain a mixture of active practicing, semi-retired and retired surveyors who enjoy supporting and encouraging the next generation of surveyors into the industry.

Assessors must be a member of RICS and an experienced Residential Surveyor and Valuer. Full training and support is given so no assessing experience is necessary.

Benefits of being an assessor with Sava include:

· Free technical CPD

· Online process allows you to work from home

· Can be fitted around other commercial activities

· Payment per completed learner is £2,600

· An opportunity to help shape the next generation of surveyors

If you would like to find out more about being an Assessor and whether this is something you would like to get involved in, then please email training@sava.co.uk for more information.